Category / Economics

Do Corporate Taxes hurt growth?

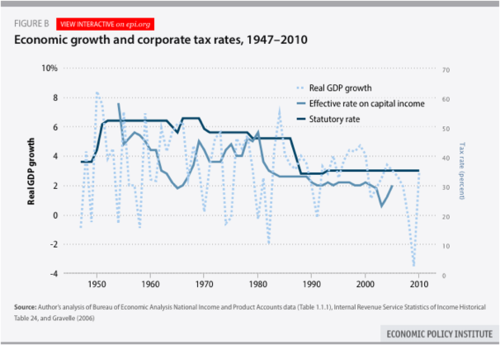

There was an interesting little blog by Dylan Matthews on the wonderful Wonkblog at the Washington Post back in June on some research by Thomas Hungerford at the Economic Policy Institute. Hungerford argues in his paper that corporate taxes do not hurt growth.

Here’s one of the relevant graphs:

However, as Matthews writes

One issue with this chart that emerges immediately is that it doesn’t control for any non-corporate tax factors that might affect economic growth, such as population growth, federal spending, Fed policy or the population’s education level. All it shows is that changes in the corporate tax rate do not drive changes in economic growth, not that the rate does not affect growth. Everyone should agree to that much; I don’t think there’s ever been a recession prompted by a sudden uptick in the corporate tax rate.

Matthews then goes through some of the countervailing evidence.

Interesting little blog anyway.

“Germany’s finance minister warns of a ‘revolution’ if Europe adopts America’s tougher welfare model”

According to the Daily Mail, back in May, Wolfgang Schäuble

said that abandoning the continent’s welfare model in favour of tougher U.S. standards would cause ‘revolution’.

‘We need to be more successful in our fight against youth unemployment, otherwise we will lose the battle for Europe’s unity,’ Schaeuble said.

While Germany insists on the importance of budget consolidation, Schaeuble spoke of the need to preserve Europe’s welfare model.

If U.S. welfare standards were introduced in Europe, ‘we would have revolution, not tomorrow, but on the very same day,’ Schaeuble told a conference in Paris.

Socialisation Yadda Yadda

{W}ithin bourgeois society, the society that rests on exchange value, there arise relations of circulation as well as of production which are so many mines to explode it. (A mass of antithetical forms of the social unity, whose antithetical character can never be abolished through quiet metamorphosis. On the other hand, if we did not find concealed in society as it is the material conditions of production and the corresponding relations of exchange prerequisite for a classless society, then all attempts to explode it would be quixotic.)

—Marx, Grundrisse

Hat Tip to Harrison Fluss.

Source: http://www.marxists.org/archive/marx/works/1857/grundrisse/ch03.htm

Taft on house prices

Good blog over at the Irish Left Review on house prices.

Here’s the important and pretty interesting graph:

He takes the data from the the Department of Environment’s Housing Statistics.

However much of the blog argues that the gap was speculative and this shows that “household debt did not become a crisis because people ‘went nuts’ buying houses”.

I find this hard to believe. A shift in house prices like this is a transfer of money from homebuyers to homeowners. Now sure, that includes property developers who bought in order to sell and obviously began with owning a lot. But it also involves people who simply owned houses, i.e. ordinary middle aged middle class ‘working people’, to use Uncle Joe‘s phrase.

We can’t explain everything by blaming the ruling class. Sometimes one section of the class gains at the expense of another. In the case of the housing bubble, homeowners gained at the expense of home buyers.

(Obvious objection, home owners still needed to own homes after they sold them. Sure, but lets imagine a couple in their 50s own a three bed family home and sell it for €500,000 to buy a smaller 2 bed for €300,000 now that their kids are grown up. Say the prices have halved so that the 3 bed is now €250,000 and the 2 bed is €150,000. The couple would still be€100,000 better off than they would have been without the bubble.)

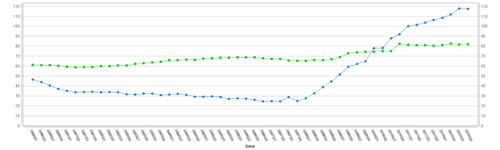

German vs Irish Debt/GDP

It is often heard from German polticians that Irish debt levels are the reasons for this problem. While every economically literate Irish person knows that’s not true.

So here’s the graph:

Ireland is blue and Germany green. Five points:

1. Germany is on a clear, slow but steady upward trajectory throughout the period. Ireland on the other hand is on a clear, slow but steady downward trajectory up until the financial crisis.

2. It is clear that Ireland’s debt problems arose because of the the crisis, they did not cause them.

3. The upper limit for debt to GDP under the Copenhagen Criteria and the Stability and Growth Pact is 60%. That is basically where Germany starts and then rises above. With the exception of 2002, Germany has been in breach of the SGP consistently since 2013.

4. The gap between Irish debt levels and German debt level today is smaller than today than they were before the crisis. German debt was roughly 30-35 percentage points higher than Irish debt before the crisis. Irish debt/GDP is roughly 25-30 percentage points higher than Irish debt/GDP before the crisis.

5. Given all of this, it is clear that Ireland’s debt problems are not because of it’s pre-crisis debt level but rather from the rate of change of Ireland’s debt during the crisis. This is important because the increase in debt, arising largely from transfer payments*, could not have been avoided. Having a lower debt level to begin with would have had no impact here. In fact there if Ireland had entered the crisis with lower debt levels the relative increase increase in its debt would have been higher not lower. Perhaps, this might have been resulted in Irish interest rates increasing higher and faster than they actually did.

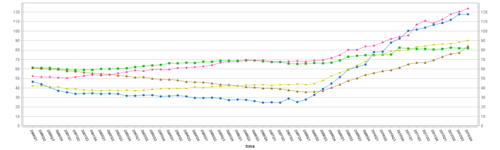

Finally, here is Spain (brown), Portugal (pink) and the UK (mustard?) added to the graph.

Again the argument for debt causing the crisis is hard to make. And the interest differential between Spain and the UK is clearly being driven, not by the debt level, but by something else…. I wonder what that could be?**

*Bank debt clearly matters here but its short run implications are actually more ambiguous than supposed.

** The answer is €

All data from Eurostat

The Great Gatsby Curve!

This is pretty great. I’ve never sen a gif like this. I came across it via Kevin Drum at Mother Jones, but it actually comes from a speech by Alan Krueger, Chairman of the Council of Economic Advisers, last year. The gif has been put together for the Whitehouse’s tumblr of all places!!!

Kalecki on Fascism

Michal Kalecki on Fascism in ‘Political Aspects of Full Employment’:

“1. One of the important functions of fascism, as typified by the Nazi system, was to remove capitalist objections to full employment.

The dislike of government spending policy as such is overcome under fascism by the fact that the state machinery is under the direct control of a partnership of big business with fascism. The necessity for the myth of ‘sound finance’, which served to prevent the government from offsetting a confidence crisis by spending, is removed. In a democracy, one does not know what the next government will be like. Under fascism there is no next government.

The dislike of government spending, whether on public investment or consumption, is overcome by concentrating government expenditure on armaments. Finally, ‘discipline in the factories’ and ‘political stability’ under full employment are maintained by the ‘new order’, which ranges from suppression of the trade unions to the concentration camp. Political pressure replaces the economic pressure of unemployment.

2. The fact that armaments are the backbone of the policy of fascist full employment has a profound influence upon that policy’s economic character. Large-scale armaments are inseparable from the expansion of the armed forces and the preparation of plans for a war of conquest. They also induce competitive rearmament of other countries. This causes the main aim of spending to shift gradually from full employment to securing the maximum effect of rearmament. As a result, employment becomes ‘over-full’. Not only is unemployment abolished, but an acute scarcity of labour prevails. Bottlenecks arise in every sphere, and these must be dealt with by the creation of a number of controls. Such an economy has many features of a planned economy, and is sometimes compared, rather ignorantly, with socialism. However, this type of planning is bound to appear whenever an economy sets itself a certain high target of production in a particular sphere, when it becomes a target economy of which the armament economy is a special case. An armament economy involves in particular the curtailment of consumption as compared with that which it could have been under full employment.

The fascist system starts from the overcoming of unemployment, develops into an armament economy of scarcity, and ends inevitably in war.”

Europe as the developing world’s supplier

Europe as the developing world’s supplier

What you might call the ‘German Strategy’

Source: European Council of American Chambers of Commerce: The Case for Investing in Europe: Why U.S. firms should stay the course by Joseph P. Quinlan, SAIS at John Hopkins and GMF: http://www.amchameu.eu/Portals/0/2012/ebooks/The-Case-for-Investing-in-Europe-AmChams-in-Europe/index.html

Percentage of world’s engineering degrees

Percentage of world’s engineering degrees.

I’m not sure how much this matters, but all the ‘China is the new America’ malarky is nonsense until China starts pushing the productivity frontier and stops ‘catching up’.

This suggests that the EU and China and the ‘Asia-8’ might not be doing too badly here.

Source: European Council of American Chambers of Commerce: The Case for Investing in Europe: Why U.S. firms should stay the course by Joseph P. Quinlan, SAIS at John Hopkins and GMF: http://www.amchameu.eu/Portals/0/2012/ebooks/The-Case-for-Investing-in-Europe-AmChams-in-Europe/index.html