“The social function of the doctrine of ‘sound finance’ is to make the level of employment dependent on the state of confidence.”

It really is amazing how good this essay is.

h/t Chris Dillow

“The social function of the doctrine of ‘sound finance’ is to make the level of employment dependent on the state of confidence.”

It really is amazing how good this essay is.

h/t Chris Dillow

As Open Europe point out, European inflation is currently at 1.1% well below the 2% target. Therefore the ECB is failing its mandate.

Just saying is all.

Monhamed El Erian, the CEO of PIMCO, has suggested NGDP targeting or shifting to Employment/Population targetting in an article for Project Syndicate. Granted PIMCO have some form for being a bit Keynesian in its policy proposals, but its still interesting to see something this radical being proposed by them.

In assessing how far it is from meeting its mandate, the Fed may be better served by shifting from unemployment to employment thresholds (for example, the employment/population ratio). It could even start moving to a more holistic operational measure (say, nominal GDP), together with indicators of the economy’s structural fragility.

A refrain heard endlessly by followers of the recent series of reforms in European economic governance is that the increased budgetary restrictions do not affect the composition of a balanced budget, but rather simply insist on a balanced budget. In the patronising and oft-heard expression: you can have a high tax-high spend government, and you can have a low tax-low spend government, but you can’t have a low tax-high spend government.

For a moment I want to ignore the fact that these restrictions don’t address the question of the cyclicality of government spending. (See recent comments by the IMFs Craig Beaumont on Ireland’s budgetary path for a contrasting approach to rule based fiscal policy.)

But putting that concern aside, there has been a widespread suspicion, especially by those of us on the ‘left’, that really these budgetary rules are about reducing social expenditure, not simply about balanced budgets.

In France, Francois Hollande has made some moves to balancing the budget by increasing tax rather than cutting social expenditure. (The permitted “high tax-high spend” option mentioned above.) But for this he has been unofficially reprimanded by Olli Rehn EU Commisioner for Economic and Financial Affairs, (i.e. the EU Finance Minister):

In an interview with the French weekly Le Journal du Dimanche, Olli Rehn, commissioner for economic and monetary affairs, said that tax levels in France had reached a “fateful point”. “Budgetary discipline must come from a reduction in public spending and not from new taxes,” he added.

While this has been mentioned already is, ahem, more widely read forums, I wanted to make a little note of it myself.

Paul Krugman asks “Where are the Austerian Economists?”

I’ve been part of a discussion over the direction of economic policy debate — as opposed to the direction of actual economic policy — in which an interesting question has been raised: which prominent economists are now making the best case for fiscal austerity? It’s a tough question to answer, because at this point it’s hard to find any prominent economists making that case.

By “prominent”, by the way, I’m trying not to make a personal judgment. I may think that [redacted] is actually not too bright, and doesn’t deserve his reputation, while I may think that [redacted] is actually a far better economist than many others with bigger professional reputations, but that’s not the question here; the question is which economists with big reputations and large citation indexes are making the austerian case.

And the answer is, it’s hard to think of any. Alberto Alesina, once the guru of expansionary austerity, is still defending his earlier research, but not playing a major role in current policy debate. Reinhart and Rogoff, whose 90-percent cliff was once gospel, are defending their professional reputations while trying to move on, but aren’t lending their voices to calls for continuing austerity. Who’s left?

Yes, you can find economists at right-wing think tanks and some international organizations making the austerian case, but again, I’m talking about economists with big independent reputations, justified or not. And I can’t think of any. That wing of austerianism has simply dissolved.

And as far as we can tell, it makes no difference. Have Paul Ryan, George Osborne, Olli Rehn, Wolfgang Schäuble changed their tune even a bit? No, they’re busy claiming one quarter of positive growth as vindication.

For those who like to think that serious economic debates matter, it has been a humbling experience.

While this might be true in the anglo-phone world. It ain’t everywhere. Hans Werner Sinn, probably the leading economist in Germany today, is still banging the Austerian drum.

Interesting little blogpost at openeurope on the belief by Handelsblatt magazine in Germany that although we don’t have inflation, it is coming.

Obviously, I pretty strongly disagree.

The has been a growing argument that as Paul Krugman puts it,

[we] seem to be seeing a general shift in the sources of rising inequality, from inequality in compensation to good old-fashioned capital versus labor.

In other words if you want to get ahead in life, don’t get an education, get rich parents. Or to put it otherwise, increasingly, people who earn loads of money don’t get paid it for their skilled labour, then earn it from returns on capital.

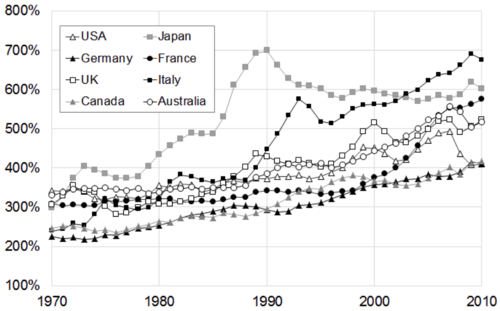

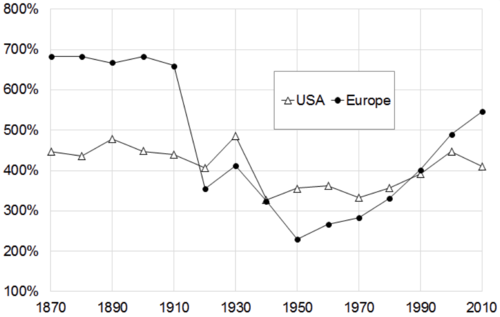

In a new VOX article, based on a paywalled (grrr) article “Capital is back: wealth-to-income ratios in rich countries, 1700-2010”, Piketty and Zucman give us a few nice graphs. I’m just C&Ping them below…

Figure 1. Private wealth / national income ratios, 1970-2010

Figure 2. Private wealth / national income ratios, 1870-2010: Europe vs. USA

Figure 3. Capital shares in factor-price national income, 1975-2010

The article that the Derek Scally putdown quote comes from actually has some interesting things to say about German lending to Ireland pre-2008.

Hibernocentric crisis narrative

That Germans saved and Irish spent in the past decade is one of those sweeping statements rarely challenged from which pundits have extrapolated their Hibernocentric crisis narrative. The Germans were effectively buying the drinks for the Irish, they say, and should thus share the blame, the cost and the consequences for the car now wrapped around the tree.The trouble is that the financial data to support this argument is at best complex and patchy and at worst far less compelling than you might think.

Last March the Central Bank supplied The Irish Times with previously unpublished data showing that when the music stopped in 2008 it was Britain, not Germany, that was by far the biggest source of funding for Irish banks.

Even the infamous bondholders were, according to consolidated data sets, a quarter Irish and two-thirds non-euro area. The entire euro area, including Germany, held just 13 per cent of total Irish bank bonds. While the data available is far from complete or perfect, it presents a different reality from that peddled by the pundits.

It’d be nice if the IT could give us links for these publications, instead of doing that weird and stupid thing that the IT and II do of linking within the website and not giving external links.

Dear Irish Print Media,The internet enables you to use links. They are the footnotes of the internet. If you want to look like a serious newsite and not some spammy viagra pill site, please, use them.

Yours etc.

Derek Scally on Irish punditry on Germany:

For anyone who has any clue, it’s like watching a piano teacher who is one lesson ahead of the student.

Frank Callanan on Fintan O’Toole writing about the Seanad:

It is in the nature of proposals for constitutional change that they throw up confederacies of opposites. Fintan O’Toole has rallied to the defence of Seanad. However, with the monotonal acridity that marks his writing on post-crash Irish politics he also pronounces that “the Seanad stinks”. He is perhaps attempting to keep himself apart from Michael McDowell and the leadership of Fianna Fáil. The Seanad’s sudden friends are a rum lot.

LOL. The IT should do more of bitchy.