The New Statesman reports that “The US Treasury is delaying a report on China’s manipulation of the yuan, which was due out on 15 April, by several months.” This has been a pretty big issue of policy debate within economics recently. China is quite clearly engaging in currency manipulation on a level never previously seen (as in never ever). The US Treasury has a statutory obligation to publish a report every year (I think) that states which, if any, countries are engaging in currency manipulation. If the US government then gets a report saying that China is manipulating the value of its currency there would be a political obligation to do something about it. This hasn’t come to a head until recently because up until the recession it was seen as China financing the US deficit. But now its seen as China importing US demand and exporting Chinese savings at a time when the US government is trying to stimulate demand and when savings are already greater than investment.

Perhaps at the for front of the debate over the renminbi is Paul Krugman. He has written a lot on this recently and has given a very interesting an informative talk with Fred Bergsten of the Peterson Institute for International Economic. Essentially Krugman is calling for a 25% sanction on Chinese imports by the US in order to force China into revaluing its currency. The response has been impassioned. Business week reports:

Morgan Stanley Asia Chairman Stephen Roach said a “baseball bat†should be taken to economist Paul Krugman over his call for the U.S. to pressure China into allowing the yuan to appreciate.

Tyler Cowen at Marginal Revolution has said that Krugman current tirade shows that he is now neither an economist not a liberal! Krugman’s calls are also being heard in China where China Daily has been condemning Krugman’s call. The best commentary that I’ve seen that criticises Krugman’s argument is that of Yiping Huang, Professor of Economics at the China Center for Economic Research, Peking University, who has a detailed article over at VOX.eu. In that article Huang argues, as have others elsewhere, that if America goes on the offensive over the renminbi, it will only make it less likely that China will revalue. The idea here is that popular opinion will prevent the Chinese government from ‘giving in’ to America if America goes on the offensive, but that if this is done diplomatically China might revalue. I’m not too sure if I buy this argument for three reasons, 1. I don’t know how responsive the Chinese government is to public opinion, 2. a revaluation could actually benefit Chinese consumers as the renminbi would be stronger, and consumers would probably consume more and save less, resulting in a jump in living standards, 3. the US has been putting diplomatic pressure on China for years now to revalue and China simply hasn’t done it.

Anyway it’s worth listening to what Krugman is saying as, judging from the fact that the Treasury seems to be preparing a significant report, it now look like America might be about to go on the offensive. Krugmanwrites:

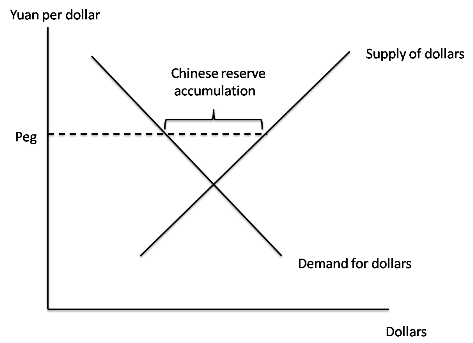

The renminbi thing isn’t at all hard to explain — it’s just supply and demand. Here:

The more depreciated China’s exchange rate — the higher the price of the dollar in yuan* — the more dollars China earns from exports, and the fewer dollars it spends on imports. (Capital flows complicate the story a bit, but don’t change it in any fundamental way). By keeping its current artificially weak — a higher price of dollars in terms of yuan — China generates a dollar surplus; this means that the Chinese government has to buy up the excess dollars. There’s nothing arcane about it.

Nor is there anything arcane about the implications: In the current environment, with high unemployment around the world and policy interest rates as low as they can go, this is a predatory, beggar-thy-neighbor policy.

In another post Krugman extends his argument:

By creating an artificial capital account deficit, China is, as a matter of arithmetic necessity, creating an artificial current account surplus. And by doing that, it is exporting savings to the rest of the world.

In normal times, you could argue that this policy provides benefits to the rest of the world, by reducing borrowing costs (although given what we did with those capital inflows, maybe not). But these aren’t normal times. We’re currently living in a world in which both central banks and governments are unable or unwilling to pursue sufficiently expansionary policies to eliminate mass unemployment; so it’s a paradox of thrift world, in which anyone who tries to save more reduces demand, reduces employment, and – because investment responds to excess capacity – ends up actually reducing investment. By exporting savings to the rest of the world, via an artificial current account surplus, China is making all of us poorer….

… it’s a mistake to focus only on direct China versus America competition. In many cases, Chinese exports compete with those of other developing nations. If the renminbi rises, those nations would become more competitive – and would also find their currencies appreciating against the dollar, offering new channels for onshoring. This may sound speculative, but it isn’t: remember, if China ends its artificial export of capital, that has to show up in trade flows one way or another.

In the same post he explains how he sees the confrontation playing out:

Here’s how the initial phases of a confrontation would play out – this is actually Fred Bergsten’s scenario, and I think he’s right. First, the United States declares that China is a currency manipulator, and demands that China stop its massive intervention. If China refuses, the United States imposes a countervailing duty on Chinese exports, say 25 percent. The EU quickly follows suit, arguing that if it doesn’t, China’s surplus will be diverted to Europe. I don’t know what Japan does.

Suppose that China then digs in its heels, and refuses to budge. From the US-EU point of view, that’s OK! The problem is China’s surplus, not the value of the renminbi per se – and countervailing duties will do much of the job of eliminating that surplus, even if China refuses to move the exchange rate.

And precisely because the United States can get what it wants whatever China does, the odds are that China would soon give in.

Look, I know that many economists have a visceral dislike for this kind of confrontational policy. But you have to bear in mind that the really outlandish actor here is China: never before in history has a nation followed this drastic a mercantilist policy. And for those who counsel patience, arguing that China can eventually be brought around: the acute damage from China’s currency policy is happening now, while the world is still in a liquidity trap. Getting China to rethink that policy years from now, when (one can hope) advanced economies have returned to more or less full employment, is worth very little.

Obviously there are a number of interesting things in here. The argument that a revaluation would benefit other Asian exporters is one I find pretty interesting but not necessarily one I’m convinced of. That said I’ve seen very little, with the exception of Huang’s article linked above, that is in anyway persuasive that Krugman is wrong. And with the being a strong appetite in Congress for taking on China (130 members of Congress signed a letter to Timothy Geithner, Treasury secretary, and Gary Locke, commerce secretary, calling for action of China’s currency manipulation. Text of the letter here), it is well worth watching how this develops.