Fourier on sexual liberation in his early 19th century socialist utopia:

Love in Harmony [i.e. the Phalanx] will be ‘free,’ but highly organized, the aim being to provide universal sexual gratification. Everyone, including the elderly and the deformed, will be assured of a ‘sexual minimum’. To effect this, philanthropic corporations composed of outstandingly beautiful and promiscuous erotic priests and priestesses will joyfully minister to the needs of less attractive Harmonians. The qualification for admission to this ‘amorous nobility’ will be a generous sexual nature, capable of carrying on several affairs at once (this will be tested under examination conditions). Polygamy and adultery will be praiseworthy in Harmony, and they will be open and unashamed – there will be no secrecy – whereas monogamy will be despised as the narrowest sort of love. Polygamy, Fourier believed, was already almost universal – though covert – in our own civilization. He drew up a list of seventy-two distinct varieties of cuckold.

In Harmony, the notion of sexual ‘perversion’ will be abandoned. Lesbians, pederasts, flagellants, and others with more recondite tastes such as heel-scratching and eating live spiders, will all have their desires recognized and satisfied, and will meet regularly at international convocations. Fourier himself confessed to a fondness for lesbians, and calculated that there were 26,400 men on earth, beside himself, who shared this abnormality.

The amorous affairs of each Phalanx will be organized by an elaborate hierarchy of officials, titled variously high priests, pontiffs, matrons, confessors, fairies, fakirs, and genies. They will hold sessions of the court of love each evening, after the children have gone to bed. In arranging relationships, they will depend on a complete knowledge of everyone’s likes and dislikes, obtained through confession, and an intricate card-index system of erotic personality-matching.

{W}ithin bourgeois society, the society that rests on exchange value, there arise relations of circulation as well as of production which are so many mines to explode it. (A mass of antithetical forms of the social unity, whose antithetical character can never be abolished through quiet metamorphosis. On the other hand, if we did not find concealed in society as it is the material conditions of production and the corresponding relations of exchange prerequisite for a classless society, then all attempts to explode it would be quixotic.)

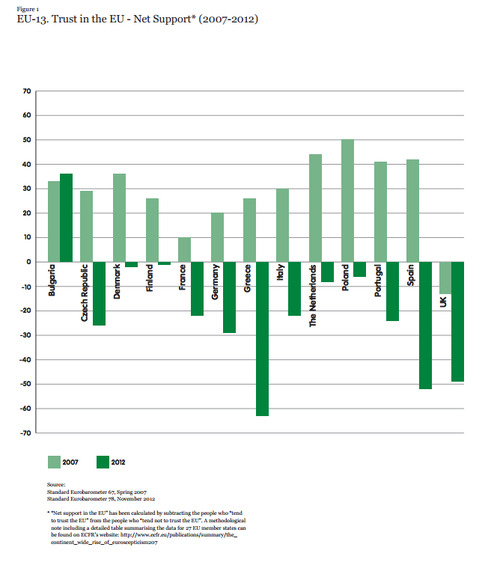

On 14 February 2010, 20 prominent economists wrote to theSunday Times in support of George Osborne’s deficit reduction strategy. They said: “… in order to be credible, the government’s goal should be to eliminate the structural current budget deficit over the course of a Parliament, and there is a compelling case, all else equal, for the first measures beginning to take effect in the 2010/11 fiscal year.” The Chancellor hailed their letter as a “really significant moment in the economic debate”.

Two and a half years later, the UK is mired in a double-dip recession and Osborne is set to borrow £11.8bn more than Labour planned. For this week’s issue of the New Statesman (out tomorrow), we asked the 20 whether they regretted signing the letter and what they would do to stimulate growth. Of those who replied, only one, Albert Marcet of Barcelona Graduate School of Economics, was willing to repeat his endorsement of Osborne. Nine urged the Chancellor to abandon his opposition to fiscal stimulus and to promote growth through tax cuts and higher infrastructure spending, while others merely said “no comment” or were “on holiday”.

“1. One of the important functions of fascism, as typified by the Nazi system, was to remove capitalist objections to full employment.

The dislike of government spending policy as such is overcome under fascism by the fact that the state machinery is under the direct control of a partnership of big business with fascism. The necessity for the myth of ‘sound finance’, which served to prevent the government from offsetting a confidence crisis by spending, is removed. In a democracy, one does not know what the next government will be like. Under fascism there is no next government.

The dislike of government spending, whether on public investment or consumption, is overcome by concentrating government expenditure on armaments. Finally, ‘discipline in the factories’ and ‘political stability’ under full employment are maintained by the ‘new order’, which ranges from suppression of the trade unions to the concentration camp. Political pressure replaces the economic pressure of unemployment.

2. The fact that armaments are the backbone of the policy of fascist full employment has a profound influence upon that policy’s economic character. Large-scale armaments are inseparable from the expansion of the armed forces and the preparation of plans for a war of conquest. They also induce competitive rearmament of other countries. This causes the main aim of spending to shift gradually from full employment to securing the maximum effect of rearmament. As a result, employment becomes ‘over-full’. Not only is unemployment abolished, but an acute scarcity of labour prevails. Bottlenecks arise in every sphere, and these must be dealt with by the creation of a number of controls. Such an economy has many features of a planned economy, and is sometimes compared, rather ignorantly, with socialism. However, this type of planning is bound to appear whenever an economy sets itself a certain high target of production in a particular sphere, when it becomes a target economy of which the armament economy is a special case. An armament economy involves in particular the curtailment of consumption as compared with that which it could have been under full employment.

The fascist system starts from the overcoming of unemployment, develops into an armament economy of scarcity, and ends inevitably in war.”

Clément Méric, an 18 years anti-fascist activist and student syndicalist activist, was declared brain-dead this morning. He was attacked in the heart of Paris by extreme-right skinheads.

A very rough translation of the statement by his union, Solidaires, is below.

On Wednesday, June 5, 2013, leaving a clothing store near the Saint-Lazare, our comrade Clement, a unionist in Solidaires Etudiant-e-s and Antifascist Action Paris-Banlieue activist, was beaten to death by members of the extreme right. The death of our comrade takes place in the context of the development of a violent fascist movement in France and elsewhere in Europe. Clement is in a brain dead state Pitié-Salpêtrière Hospital due to his injuries.

His loss overwhelms us. Our pain and anger are compounded by the certainty that there are very many, antifacist activists and people exposed to homophobia and/or racism, who could and can still be victims.

Today all our thoughts are with his family, his loved-ones and his comrades in Solidaires Etudiant-e-s with whom we express our solidarity.

This heinous act is inseparable from the increase in racist attacks by homophobic right-wing extremists over the past months and the creation of a climate of hatred, which is maintained by political speeches condemning not exclusive of the National Front and fascist factions.

Beyond the police and judicial action, it is time to strengthen the anti-fascist movement. With Solidaires Etudiant-e-s, the Solidaires union calls on all those who condemn this heinous act and refuse to tolerate the extreme right vermin to participate massively in many rallies today and in the coming days in Paris and in the provinces. This includes the demonstration tonight Thursday, June 6 from 17 h in front of the passage of Havre Saint Lazare metro and then join the Saint Michel 18 H 30.

Herman Van Rompuy has circulated the draft agenda of the European Council meeting, which takes place today and tomorrow, 18-19 October 2012, in Brussels. It lists three items for discussion: Economic Policy, Strategic Partners, and Other Items. In the draft conclusions, which have been leaked, the last agenda items combined take up roughly less than a page of the ten-page text. It seems clear that, as has been common for European Council meetings since the Greek crisis erupted in late 2009, this Council meeting will be focused on economic policy.

In the draft agenda, Van Rompuy names a number of economic policy issues to be discussed, following up on the outcomes of the June European Council (28-29 June 2012). He will present his Interim Report on “Towards a Genuine Economic and Monetary Union”, developed with the Presidents of the European Commission, European Central Bank and Eurogroup in consultation with the Member State capitals, which deals with “the wider issue of the Banking union and its components”. Progress in the implementation of the Compact for Growth and Jobs, which is appended to the Conclusions of the June European Council, will be reviewed. In the leaked conclusions of the forthcoming Council, there is a detailed discussion of progress on the various points of the compact. Most of the discussion at the Council, however, is likely to focus on the Interim Report, in which there are a number of controversial proposals.

Single Supervisory Mechanism and Banking Union

The report highlights the proposed bank recovery and resolution directive, the proposal on deposit guarantees and the proposal, made in September by the Commission, to establish a “single supervisory mechanism hosted by the European Central Bank, covering the euro area and open to all Member States”. The report states that this move towards a banking union is a “matter of priority”, while the draft conclusions go further, calling for all the above proposals to be agreed by the end of the year at the latest, with the SSM up and running on 1 January 2013. It is worth noting Berlin’s recent objections that this time frame is too short.

Integrated Budgetary Framework and Economic Governance

The report proposes further moves on European budgets under three headings. The first address “Stronger Economic Governance”, which refers to the increased supervisory powers of the EU over national budgets through the six-pack, the European Semester, the Treaty of Stability, Coordination and Governance and the proposed two-pack. The second heading is “Fiscal Capacity”. This is what the Financial Times calls ‘eurospeak’ for a Eurozone budget. The final heading refers to the still-present idea of eurobonds. Interestingly, the German idea of a redemption fund is mentioned under this heading.

The newest of these proposals is clearly the proposal for a Eurozone budget. The report is careful to distinguish the “fiscal functions”, which would fall under a Eurozone budget, from the EU-wide Multiannual Financial Framework (the EU’s long term budget that sets out expenditure ceilings under a number of headings). These new fiscal functions are described in the following manner:

“One of the functions of such a new fiscal capacity could be to facilitate adjustments to country specific shocks by providing for some degree of absorption at the central level. In the EMU, the response to a symmetric shock affecting all countries simultaneously should primarily be provided by monetary policy, whereas in the context of country-specific economic shocks, the response falls primarily on national budgets…Another important function of such a fiscal capacity would be to facilitate structural reforms that improve competitiveness and potential growth in relation to an integrated economic policy framework…the two objectives of shock absorption and support to structural reforms are complementary and mutually reinforcing.”

These two functions, “shock absorption and support to structural reforms”, are clearly very far reaching and could allow for a very substantial Eurozone budget. Indeed, Pierre Moscovici, the French Finance Minister, has advocated that the provision of some unemployment insurance be taken on at a European level through this kind of Eurozone budget. If this kind of fiscal responsibility was delegated to a European level it would qualitatively shift the nature of the EU’s intervention in social and economic life. Interestingly, the idea of a Eurozone budget is something that Germany has supported, with Germany saying that it would be happy with a Eurozone budget providing funding for active labour market policies (retraining programmes etc). Even the UK’s Conservative party has recently supported the idea of a Eurozone budget.

On the question of furthering the integration of economic governance, both the report and the draft conclusion point to the increased integration and supervision of national budgetary coordination, through the implementation of the Six-pack, the European Semester, the Treaty of Stability, Coordination and Governance and the agreement and implementation of the two-pack. The draft conclusions invite legislators to ‘find agreement’ on the two-pack ‘by the end of the 2012 at the latest’. However, here as well there is a significant structural innovation proposed. This innovation is the suggestion that “euro area Member States… enter into individual arrangements of a contractual nature with the EU institutions on the reforms promoting growth and jobs these countries commit to undertake and their implementation.”

The Financial Times reports that, “according to officials involved in the discussion, the idea is to sign all 17 Eurozone governments to deals similar to the economic reform and restructuring plans currently required only of bailout countries”. They explain that the plan that “would require all 17 Eurozone members to sign on to the kind of Brussels-approved policy programmes and timelines now negotiated only with bailout countries. If adopted, the plan could help to meet demands in Germany for tighter control over the economies of highly indebted countries such as Italy and France”.

Notably, it is stated in Van Rompuy’s report that these budgetary “coordination mechanisms could be open to the Member States that have not yet adopted the euro”. This is in addition to the aforementioned reference in the report to the SSM being for “the euro area and open to all Member States”. These would seem to be explicit attempts to move reform of the Eurozone away from creating a two-tier Europe.

Democracy

As some readers may have noticed, the above description of the Interim Report has covered three of the ‘four building blocks’ found in Van Rompuy’s June report: banking integration, budgetary integration and the integration of economic governance. This leaves the question of democratic legitimacy and political union. On this question, IIEA Researcher Linda Barry has produced a comprehensive consideration of the debates on this question. However, on the issue of addressing the problem of democratic legitimacy at a European level, the Interim Report offers little more than vague injunctions that the European Parliament and national parliaments should play a more important role. For example, it argues, “ways to ensure a debate in the European Parliament and in national parliaments on the recommendations adopted in the context of the European Semester should be explored.” This lack of detail when compared with the other building blocks conveys an implicit sequencing for the actions – economic and financial reforms will take precedence in the immediate term, with political reforms and deepened political integration to be considered later.

Going Forward

It is obviously yet to be seen what the reception of the Interim Report will be at this week’s European Council meeting and how the final conclusions will differ from the leaked draft conclusions.

One thing that is clear is Van Rompuy’s proposal in the Interim Report that building on his “report and taking into account the exchange of views at the 18-19 October European Council and its conclusions, a specific and time-bound roadmap for the achievement of a genuine Economic and Monetary Union will be presented at the 13-14 December European Council.”

On Wednesday 1 August 2012, the Irish Government began the final stage of ratifying the Treaty establishing the European Stability Mechanism (ESM).

The ESM treaty is a stand alone treaty, which establishes the ESM. The ESM will provide financial assistance to members of the Eurozone and replaces existing temporary funding programmes the European Financial Stability Facility (EFSF) and the European Financial Stabilisation Mechanism (EFSM). Along with the Treaty on Stability, Coordination and Governance (TSCG), the ESM treaty was signed earlier this year.

The ESM treaty had already been passed by the Dáil (20 June 2012), the Seanad (27 June 2012) and had been given Presidential Assent (3 July 2012). However, due to a challenge brought to the Supreme Court of Ireland by Thomas Pringle, an independent TD for Donegal South-West, the Government did not complete the process of ratification. On Tuesday 31 July, the Supreme Court rejected Mr Pringle’s claim that the ESM Treaty is unconstitutional and cannot be ratified without a referendum. The Government then lodged the documents required to complete the ratification process with the General Secretariat of the Council of the EU. Once the General Secretariat of the Council has processed these documents, the treaty will have been ratified by Ireland.

The Treaty enters into force as soon as it is ratified by signatories whose initial subscriptions collectively represent 90% of the total subscriptions. Therefore, the treaty cannot be ratified until all countries whose initial subscriptions are greater than 10% of the total ratify it. Ireland’s initial subscription is only 1.592% of the total. In Italy, whose initial subscription to the ESM is 17.914%, the Treaty was given Presidential Assent on 23 July 2012, leaving only the final step of the General Secretariat of the Council of the EU receiving and processing the documents to complete Italy’s ratification process. Consequently, Germany is the last remaining country whose ratification is required for the Treaty to enter into force. Germany’s initial subsription is 27.146% of the total. The German Bundesrat and Bundestag passed the Treaty on 29 June 2012 but due to a constitutional challenge Germany’s ratification has been deferred until after a decision by Germany’s constitutional court on 12 September 2012.

Estonia has also not completed its ratification process, however, as Estonia’ s contributions amount to 0.186% of the initial subscriptions, the Treaty can enter into force without Estonia.

The Treaty on Stability, Coordination and Governance builds on already existing EU legislation, therefore it is worth considering which aspects of the Treaty’s Fiscal Compact are new. This article examines the provisions contained in the Fiscal Compact. The first half of this article considers the four fiscal rules and shows that none are new. The second half considers the enforcement mechanisms in the Treaty and finds that some new and some are not new. A summary of what’s new and what’s not is detailed in Table 1 below.

Not New

New

The rule that Debt-to-GDP ratio should be 60% or less

Expanded use of reverse qualified majority voting

The rule that Government deficits should be 3% or less

The requirement for the introduction of automatic correction mechanisms on a national level

The rule that Government structural deficits should be 0.5% or less

The requirement to transpose the fiscal rules into national law

The rule that if the debt-to-GDP is “significantly below 60% and where risks in terms of long-term sustainability of public finances are low” the structural deficit can be up to 1.0%

The role of the Court of Justice of the European Union in ensuring that these rules are transposed into national law

The allowance for temporary deviations from a country’s medium term objectives in ‘exceptional circumstances’

The provisions to ex-ante report on public debt issuance

The requirement for a 1/20 reduction in debt per year if a country has a debt to GDP ratio over 60%

The creation of budgetary and economic partnership programmes

Reverse qualified majority voting on sanctions

Table 1: What’s new and what’s not in the Fiscal Compact?

Introduction

Most of the provisions contained in the Treaty on Stability, Coordination and Governance concern fiscal policy. These provisions are contained in Title III of the Treaty, which is entitled the ‘Fiscal Compact’ and are probably the most widely discussed aspect of the Treaty.

It is worth noting that the Treaty’s rules on fiscal policy do not say anything about what governments can or should spend on, nor about how much a government can or should spend. The rules only relate to the size of the government deficit and the size of the country’s debt burden.

Although the provisions on fiscal policy are so important that some have referred to the Treaty as the Fiscal Compact, attention should also be paid to Title IV and Title V of the Treaty. Title IV comprises provisions for increased economic policy coordination and convergence and Title V sets out new rules for the governance of the Eurozone. This article will only address Title III, the Fiscal Compact.

The purpose of this article is to give some background to the provisions contained in the Fiscal Compact, as many of them are not new. It demonstrates that even those measures that are new are, by-and-large, relatively minor changes to existing law.

I: The Four Fiscal Rules

The Fiscal Compact contains both a number of restrictions on budgetary policy and details of how these restrictions are to be enforced. The four main restrictions are

1.Debt-to-GDP ratio should be 60% or less;

2.Government deficits should be 3% or less;

3.Government structural deficits should be 0.5% or less

4.If the debt-to-GDP is “significantly below 60% and where risks in terms of long-term sustainability of public finances are low” the structural deficit can be up to 1.0%

None of these restrictions are new.

The 60% debt rule and the 3% deficit rule

The 60% debt rule and the 3% deficit rule are long established. They constitute one of the four ‘Convergence Criteria’ contained in the Maastricht Treaty, which came into effect on 1 November 1993. The Convergence criteria are criteria that European Union Member States have to fulfill in order to adopt the euro as their currency.

Article 104c of the Maastricht Treaty also states “Member States shall avoid excessive government deficits”. The Maastricht Treaty also requires that Member States exercise “compliance with budgetary discipline on the basis of the following two criteria: (a) whether the ratio of the planned or actual government deficit to gross domestic product exceeds a reference value… (b) whether the ratio of government debt to gross domestic product exceeds a reference value… The reference values are specified in the Protocol on the excessive deficit procedure annexed to this Treaty.” The reference values are the 60% debt rule and the 3% deficit rule.[i]

These rules were further advanced four years latter in the Stability and Growth Pact (SGP). The SGP was a set of agreements made in 1997 between the Member States of the EU. It has since been developed substantially. The aim of the SGP was to ensure that the economies of the EU remained in healthy fiscal positions. It was believed that this was necessary for the stability of the Euro, which was to be introduced two years later. The two main provisions of the SGP were, once again, that countries should have a budget deficit no higher than 3% of GDP and a debt to GDP ratio no higher than 60% of GDP.

The SGP was set out in a European Council resolution in June 1997 and in two major pieces of legislation: regulations[ii]1466/1997 and 1467/1997[iii]. Regulation 1466/1997 is known as the Stability and Growth Pact’s ‘preventative arm’ because it sets out a multilateral surveillance system through which country’s budgetary positions are observed in order to prevent countries from developing deficits greater than 3% of GDP or debt to GDP ratios greater than 60%. A significant part of this is that it requires each country to specify a medium term budgetary objective.

Regulation 1467/1997 is known as the Stability and Growth Pact’s ‘corrective arm’ because it sets out how a country should correct their fiscal position if they have deficits greater than 3% of GDP or debt to GDP ratios greater than 60%. It provides for an ‘excessive deficit procedure’ that should be implemented if countries are not achieving the aims of the SGP.

Revisions to the Stability and Growth Pact

The Stability and Growth Pact has been developed significantly since 1997. The pact was heavily amended in 2005 to allow for deviations from a country’s medium term objectives. The post-2005 SGP is often referred to as ‘the Revised Stability and Growth Pact’.

Over the last year a further series of reforms to develop the SGP has been going through the EU institutions. Firstly there was the six pack. The six pack contains five regulations and one directive. The six pack came into effect on 13 December 2011.

Finally there is the twopack. The two pack contains two regulations proposed by the European Commission on 23 November 2011. However, they are awaiting adoption by the Council and it is expected that they will be adopted following any amendments that the European Parliament may put forward. The two pack provides for stronger surveillance of Eurozone countries’ national budgets and more oversight of the economic policy plans of those in financial difficulties.

It is worth emphasising that the six pack, unlike the Treaty on Stability, Coordination and Governance and the two pack, is not currently being debated. It is already law and has been in force since December 13 2011.

The 0.5% and 1% Structural Deficit Rules

The 0.5% and 1% structural deficit rules are contained in both the Treaty on Stability, Coordination and Governance and in the six pack.

The Treaty on Stability, Coordination and Governance commits those who ratify the Treaty to a ‘balanced or in surplus government’ budget. The Treaty says this commitment is respected “if the annual structural balance of the general government is at its country-specific medium-term objective, as defined in the revised Stability and Growth Pact, with a lower limit of a structural deficit of 0,5 % of the gross domestic product at market prices.” Furthermore, it states that this medium term objective can be no higher than 0.5% of GDP. Importantly this provision is not new. It is contained in Regulation 1175/2011, one of ‘the six pack’ that were agreed in Winter 2011. Regulation 1175/2011 amends Regulation 1466/97; the ‘preventative arm’ of the SGP mentioned above. Just as the 0.5% deficit rule is not new, the 1% structural deficit rule is not new. The 1% deficit rule is contained in the Treaty on Stability, Coordination and Governance where it states that if a country’s debt to GDP is “significantly below 60 % and where risks in terms of long-term sustainability of public finances are low” the structural deficit can be up to 1.0%.

Both the 0.5% and 1% structural deficit rules, are contained in Regulation 1175/2011, where it amends articles 2(a) and 5 of Regulation 1466/97, the ‘preventive arm’ of the SGP. As emphasized above, this regulation is already law.

What’s new in the four main restrictions?

Given the European legislation already in place, it is worth considering what aspects of the Treaty on Stability, Coordination and Governance’s four restrictions on fiscal policy are new. The answer is none. The 60% debt rule and the 3% deficit rule have a part of EU Treaty law since the Maastricht Treaty came into force in November 1993 and the 0.5% and 1% structural deficit rules have been in force since December 2011.

Of course this does not mean that nothing in the Treaty is new. However, the novelties in the Fiscal Compact relate to how the fiscal rules are enforced, not to their content.

II: Enforcement of the Four Fiscal Rules

Transposition of the Budget Rule into National Law and the Court of Justice

Probably the most significant original piece of law in the Fiscal Compact part of the Treaty, and perhaps in the entire Treaty, is the requirement for national governments to transpose the fiscal rules into their national law. The Treaty establishes an “obligation to transpose the "balanced budget rule" into their national legal systems, through binding, permanent and preferably constitutional provisions”. The Treaty also provides for an independent body at national level to be established to monitor their implementation.

Also new is the role of the Court of Justice of the European Union (CJEU) in this process. There is much confusion on this topic but the issue is relatively simple. The Treaty states that if a country fails to transpose the balanced budget rule into national law they can be brought before the CJEU and directed to do so. If the country fails to comply with the court’s directions, as a last resort, the country can be fined up to a maximum of 0.1% of GDP. (Note that the CJEU is not given a remit in the Treaty to decide if a country has breached the fiscal rules.)

In the Event of Deviations from the Medium Term Objective

The Treaty on Stability, Coordination and Governance follows on from previously existing law, specifically Article 5 of the preventative arm of the SGP, Regulation 1466/97, in allowing for temporary deviations from the medium term objective. These temporary deviation are only allowed in the “exceptional circumstances” of “an unusual event outside the control of the Contracting Party concerned which has a major impact on the financial position of the general government or to periods of severe economic downturn as set out in the revised Stability and Growth Pact, provided that the temporary deviation of the Contracting Party concerned does not endanger fiscal sustainability in the medium-term.”

Outside of these “exceptional circumstance” in the event of a ‘significant observed deviation’ from medium term objectives, an automatic ‘correction mechanism’ will be triggered. This provision is new. It states that the correction mechanism will work on a national level “on the basis of principles to be proposed by the European Commission”. The European Commission has yet to propose these principles.

In addition to the above correction mechanism the Treaty has a provision for a 1/20 reduction in debt per year if a country has a debt to GDP ratio over 60%. This provision is not new. It is the exact same as that provided for by Regulation 1467/97 as amended by Regulation 1177/2011.

Excessive Deficit Procedure

There are also a number of new provisions on the operation of the excessive deficit procedure in Treaty on Stability, Coordination and Governance.

Reverse Qualified Majority Voting

One issue that has received some commentary is the introduction of reverse qualified majority voting in the Treaty. Reverse qualified majority means a qualified majority needs to vote against something to stop it from happening as opposed to a qualified majority voting for something to make it happen. Some have expressed concern about the legality of the reverse qualified majority voting provisions, with Peadar O’Broin stating, “The use of reverse majority is not provided for in the EU Treaties. This alteration directly by-passes the Treaty change procedures contained in Article 48 TEU, and may therefore be held inconsistent with the EU Treaties in case of a legal dispute.”

However, reverse qualified majority voting is not new. It has been introduced for a number of issues under the six pack, but the Treaty on Stability, Coordination and Governance makes its use slightly more general. The provision regarding reverse qualified majority voting is in Article 7 of the Treaty on Stability, Coordination and Governance. It involves a commitment of Eurozone countries “to supporting the proposals or recommendations submitted by the European Commission where it considers that a Member State of the European Union whose currency is the euro is in breach of the deficit criterion in the framework of an excessive deficit procedure”. However, this obligation does not apply if a qualified majority votes against the proposals or recommendations. Exactly what the ‘proposals or recommendations’ in the article could be is left open. One obvious example would be a proposal to impose sanctions.

The six pack provides for the use of reverse qualified majority voting for the imposition of sanctions. Regulation 1173/2011 on the effective enforcement of budgetary surveillance in the euro area, states “When taking decisions on sanctions, the role of the Council should be limited, and reversed qualified majority voting should be used.” On this basis the regulation details a number of sanctions that where reverse qualified majority will apply. These include, in order of severity and imposition, lodging “with the Commission an interest-bearing deposit amounting to 0,2 % of its GDP in the preceding year”, lodging an non interest-bearing deposit in the same manner and of the same amount and having a fine imposed of the same amount,

Similar rules regarding sanctions and reverse qualified majority voting apply in Regulation 1174/2011 on enforcement measures to correct excessive macroeconomic imbalances in the euro area. This regulation “lays down a system of sanctions for the effective correction of excessive macroeconomic imbalances in the euro area” and only applies to countries in the Eurozone. It enables the council to impose sanctions of an interest-bearing deposit and an annual fine by reverse qualified majority voting.

A further example of reverse qualified majority voting exists in Regulation 1176/2011 on on the prevention and correction of macroeconomic imbalances. The Commission can make recommendations on establishing that a country has not complied its recommended actions to correct its macroeconomic imbalances. These reccomendations are “deemed to have been adopted by the Council, unless it decides, by qualified majority, to reject the recommendation within 10 days of its adoption by the Commission.”

The second provision is the creation of ‘Budgetary and Economic Partnership Programmes’ which, the Treaty says a country in excessive deficit procedure will put in place. This is a new provision. The Treaty states, “The content and format of such programmes shall be defined in European Union law”. The legislation that will define the ‘content and format of such programmes’ has not yet been brought into effect. It is likely that the Budgetary and Economic Partnership Programmes in the Treaty on Stability, Coordination and Governance will relate to the ‘Macroeconomic Adjustment Programmes’ provided for in the proposal for regulation on ‘common provisions for monitoring and assessing draft budgetary plans and ensuring the correction of excessive deficit of the Member States in the euro area’. This proposed regulation is one of the two pack and lays out plans on operation of ‘enhanced surveillance’ and the operation and surveillance of countries in ‘Macroeconomic Adjustment Programmes’.

What’s new and what’s not

So in conclusion: What’s new and what’s not?

The 60% debt rule, the 3% deficit rule, the 0.5% and 1% structural deficit rules are not new. The allowance for temporary deviations from a country’s medium term objectives in ‘exceptional circumstances’ is not new. The 1/20 rule is not new. Reverse qualified majority voting is not new but its use is expanded slightly under the Treaty. The requirement for the introduction of automatic correction mechanisms on a national level is new but the principles that will form the basis of these mechanisms have not yet been proposed. The requirement to transpose the fiscal rules into national law is new, as is the role of the Court of Justice of the European Union in ensuring that these rules are transposed into national law. And finally the provisions to ex-ante report on public debt issuance and the creation of budgetary and economic partnership programmes are both new but are related to the two pack proposals.

Many of the provisions contained in the Fiscal Compact are not new. None of the four restrictions on fiscal policy are new. And, by-and-large, those measures that are new are relatively minor changes to existing law.

[ii] Regulations are one of the main forms of secondary EU law.

[iii] The Regulations linked to here are not the original regulations. They are the regulations as amended by the ‘Revised Stability and Growth Pact’ in 2005 and the ‘six pack’ in 2011.

At the informal dinner of Heads of State or Government on 23 May 2012 Franco-German differences on eurobonds figured highly. Chancellor Merkel argued eurobonds were illegal under current EU law, and others have expressed concern about their legality under German law. However, the French President, Francois Hollande, has insisted that eurobonds remain on the table, although he acknowledged “a number of countries were totally hostile, others considered this in the long term and yet other countries considered that it could be feasible at a closer date.” This was echoed by An Taoiseach, Enda Kenny, stating, “people were clear that [developing eurobonds] would be a very long process indeed”.

The proposed eurobonds are bonds issued jointly by all 17 Eurozone Members States. They are proposed as a tool to be used in dealing with the eurocrisis. Calls for the creation of eurobonds have been growing stronger. Last summer Reuters conducted a poll and found that 41 out of 59 economists polled believed that eurobonds would be a good ‘long-term solution to resolving the crisis’, although a smaller number expected euro zone leaders to agree to their establishment. Calls for eurobonds have come from a wide variety of places.The Economistpoints out that former EU Commissioner,Mario Monti, investorGeorge Soros, former German Finance Minister and prominent member of the opposition, Peer Steinbrück, have all called for them. More recently, here at the Institute of International and European Affairs, Charles Dallara, Managing Director of the IIF, has called for their creation, as did Professor Maurice Obstfeld of the University of California, Berkeley.

Opposition to eurobonds has been very strong in Germany. Hans Werner Sinn, President of one of Germany’s largest economic research institutes and a very prominent economic commentator in Germany, went as far as to say“eurobonds would destroy the euro zone”. Opinion pollsshowthat German’s overwhelmingly oppose the proposed eurobonds.

The intransigence of German opposition has meant that, until recently, negotiations on eurobonds at a European level have not made much progress. The major exception to this is the publication of a Green Paper by the European Commission on eurobonds on 23 November 2011[i]. It is likely that this paper will be the basis of any future negotiations on the issuance of eurobonds.

With the election of Francois Hollande as President of France, calls for eurobonds have been given a real boast. His support adds to a growing majority of European states that are in favour of the creation of eurobonds. Mario Monti, the Italian Premier, said of this week’s informal meeting, “A majority of countries said they were in favour of eurobonds, even those not in the Eurozone, like Britain”. The momentum for a change in European policy concerning eurobonds has been further boosted by calls from theOECDfor their creation and with signs from last weeks G8 conference in Camp David that Obama is getting behind Hollande in his disagreement with Merkel.

However, the Franco-German conflict should not be overstated, nor should Germany’s isolation on this issue. Germany has been supported in their opposition to eurobonds by Netherlands, Finland and Austria. Despite the divergence of opinions on eurobonds, Merkel described the negotiations as balanced. “We spoke differently about eurobonds. I said we need greater economic co-ordination in Eurozone and that we see considerable difficulties when we think of the fiscal treaty what possibilities exist to shape the treaties,” she said.

On this point European Central Bank President, Mario Draghi, supported Merkel saying eurobonds made sense “only when you have a fiscal union”. This sentiment echoed comments last August by European Council President, Herman Van Rompuy. “We could only have eurobonds the day when there is truly a real budgetary convergence, the day when everyone is running a balanced budget or practically a balanced budget. That’s when we could have a eurobond. But not before,” he said.

Instead of eurobonds, Germany is supporting the proposal for project bonds. Project bonds are a proposal for the EU to support specific investment projects. The European Investment Bank would invest in the riskiest element of privately issued bonds thereby making the rest of the debt appear safer and allowing it be securitised at an investment grade.Notable progress has been made on project bonds recently. President of the Commission, José Manuel Barroso, said that “concrete action for targeted investment, project bonds” had been discussed and that these discussion went much further than in October 2011, when many were against a similar proposal. He said that on Tuesday, 22 May 2012, “an agreement between the Council and the Parliament to launch a pilot phase for project bonds” was reached.

However, Enda Kenny has not shown much enthusiasm about the project bonds proposals. The Irish Times reports he “described proposals for the creation of project bond as fine, but warned that they needed to be flexible for smaller countries and should not just be confined to trans-continental projects.”

Despite the changes and development on eurobonds, no real change in policy took place at this week’s informal dinner. Nor was it intended for any real change to be achieved, the aim was rather to facilitate communication in advance of the European Council on 28/29 June, where the Greek situation and eurobonds will be discussed.

[i] In this document eurobonds are referred to as ‘stability bonds’.